The problems with Bitcoin

At approximately 62,000 euros per bitcoin as of the 8th of March 2024, the most well-known cryptocurrency is at its record high, but there are good reasons why anyone should think very carefully before buying bitcoins and why regulated financial advisers prefer diversified investment portfolios (actively or passively managed). This blog post will list some of the reasons why the future for Bitcoin might not be so bright (orange or not!) and why there remains some hope for cryptocurrencies and digital asset technologies.

Problem 1: The supply of cryptocurrencies is not really limited

People say that cryptocurrencies are limited by their coin creation methods, such as proof of work for digital coins like Bitcoin and proof of stake for coins like Ethereum, but almost anyone can create a cryptocurrency, we are not dealing with physical assets with a real limited supply, or software protected by patents and strong copyright laws.

Problem 2: Bitcoin lacks usefulness to explain its demand, besides as a vehicle for speculation.

The value of an investment is based on the present value of its future cash flows, but Bitcoin doesn’t produce any dividends like a company share and nor does it produce interest like a bond. Neither does Gold, you may say, but at least gold can be used to make things. What about government backed currencies such as the US dollar? Traditional currencies are extremely useful for payments whereas Bitcoin is slow for payments. These concerns are also shared by economists at the European Central Bank.

Problem 3: The volatility of Bitcoin

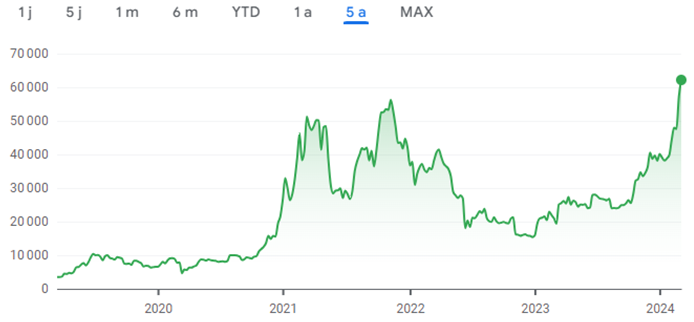

To give you an idea of just how volatile the price of Bitcoin can be, here is a five year chart as of the 8th of March 2024:

This shows that a little over a year ago at the start of January 2023, Bitcoin was worth just over a quarter of today’s value. How would you feel if Bitcoin drops back down to its January 2023 value? How would you feel if your investments were to fall by 75%, which is possible. Between November 2022 and the end of November 2023, Bitcoin lost approximately 72% of its value. The values of other digital assets, such as non-fungible tokens, have also collapsed.

Problem 4: Regulatory risk due to environmental damage and money laundering concerns.

Proof-of-work coins such as Bitcoin have increased energy consumption. A proof of work coin involves the use of mass computing power in order to crack a code which issues a new digital coin to the participant who cracked the code. These users are known as “miners” and Bitcoin miners currently consume more electricity than most countries. Bitcoin and cryptocurrencies have also been linked to money laundering and the funding of criminal activities. These factors increase the risk that regulators will “crack down” on Bitcoin and other cryptocurrencies, especially Proof-of-work coins. Some cryptocurrency and digital asset company directors have also stolen investors’ money, such as former “crypto king” Sam Bankman-Fried.

Is it always bad to invest into Bitcoin and cryptocurrencies?

Whilst I cannot give financial advice over a blog post, there are reasons why the future for digital currencies is not all bad. Firstly, Ethereum (ETH), a different cryptocurrency, recently cut approximately 99.99% of its emissions by moving from a proof-of-work coin generation method to a proof-of-stake one. Such a change may never happen with Bitcoin, but it is important to state that not all cryptocurrencies produce lots of emissions.

Secondly, on the 10th of January this year (2024), the American investment and securities regulator, the SEC, approved the first Bitcoin ETFs, which should offer a safer way to invest in terms of protection against fraud and they might make sense for some high-risk investors as part of a diversified portfolio.

Thirdly, the technology behind Bitcoin and other digital assets, Blockchain, actually has some real world uses and may make sense for international transactions, especially low frequency ones. There are many problems with Bitcoin, but the future for digital assets and blockchain may also have some opportunities.

The views expressed in this article are not to be construed as personal advice. Therefore, you should contact a qualified, and ideally, regulated adviser in order to obtain up-to-date personal advice with regard to your own personal circumstances. Consequently, if you do not, then you are acting under your own authority and deemed “execution only”. Additionally, the author does not accept any liability for people acting without personalised advice, who base a decision on views expressed in this generic article. Importantly, this article is dated and is based on legislation as of the date. It should be noted that legislation changes, but articles are rarely updated. Sometimes a new article is written; so, please check for later articles. Additionally, check for changes in legislation on official government websites. Finally, this article should not be relied on in isolation.